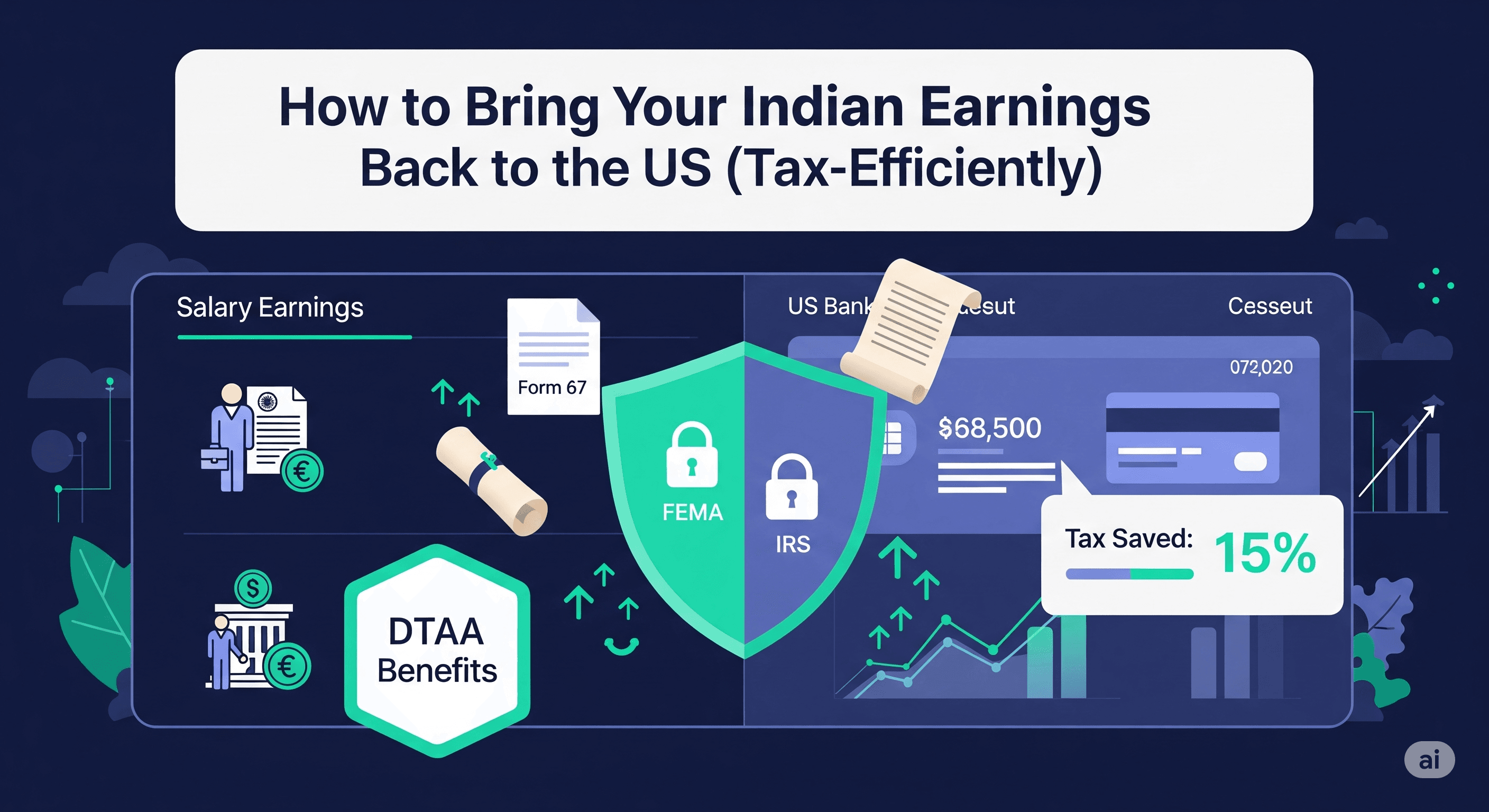

If you’re an NRI, chances are you still have financial ties in India, maybe you sold a property, received rental income, or cashed out investments. But bringing this money back to the US isn’t as simple as wiring funds.

This guide breaks down the two legal pathways of repatriation (NRE vs NRO), the paperwork involved, and most importantly, how to avoid double taxation under the India–US DTAA (Double Taxation Avoidance Agreement).

👉 Think of this as your step-by-step playbook for moving money from India to the US with minimal tax leakage.

The Two Paths of Repatriation , NRE vs. NRO

When you hold funds in India, where they sit determines how easily you can bring them back.

The Easy Path: Repatriating from an NRE (Non-Resident External) Account

- Why it’s easy: Funds in an NRE account are sourced from foreign earnings already transferred into India.

- Process: A simple instruction to your bank is enough to wire it back to your US account.

- Limits: None, both principal and interest are freely repatriable.

- Taxation: Completely tax-free in India.

✅ Example: You earned $50,000 in the US, transferred it to India, and kept it in your NRE account. You can move it back anytime without Indian tax implications.

The Regulated Path: Repatriating from an NRO (Non-Resident Ordinary) Account

- Why it’s complex: NRO accounts hold Indian-sourced income, rent, dividends, capital gains, salary, or inherited money. These are taxable in India before repatriation.

- Extra steps: Banks will not remit funds until proof of taxes paid is provided.

The $1 Million USD Limit

You can remit up to $1 million per financial year (April–March) from your NRO account, after taxes.

The Mandatory Paperwork: Form 15CA & 15CB

- Form 15CA: Your online declaration to the Indian Income Tax Department confirming remittance details.

- Form 15CB: A certificate from a Chartered Accountant (CA) verifying that all Indian taxes on the funds have been discharged. Required for most transactions exceeding ₹5 lakh.

👉 Without these forms, your bank won’t process the transfer.

Common Repatriation Scenarios (Real-World Examples)

Scenario 1: Selling Property in India

- Bought with NRE funds → Sale proceeds can go back to your NRE account, making repatriation simple.

- Inherited or bought with Indian income → Proceeds land in your NRO account and must pass through the $1M cap + 15CA/CB process.

- Tax angle: Capital Gains Tax (long-term or short-term) must be paid before funds are remitted.

Scenario 2: Repatriating Gains from Mutual Funds or Stocks

- Proceeds are first credited to your NRE or NRO account after TDS.

- If credited to NRE → freely repatriable.

- If credited to NRO → subject to limits, paperwork, and tax clearance.

Scenario 3: Repatriating Rental Income or Dividends

- Always credited to NRO accounts.

- Needs Form 15CA/CB + compliance with the $1M annual ceiling.

- Tax deducted at source (TDS) already applies in India, which you can later claim as a credit in the US.

The “Tax-Efficiently” Secret – Avoiding Double Taxation in the US

Wire Transfers Are Not Taxable Events

A common misconception is that the IRS taxes wire transfers. Not true. Only the underlying income (capital gains, rent, dividends) is taxable in the US — not the act of moving your money.

The Foreign Tax Credit (FTC) – Your Best Friend

The India–US DTAA ensures you don’t pay tax twice on the same income.

- If you’ve paid taxes in India, you can claim a Foreign Tax Credit (FTC) on your US tax return.

- Example: You paid ₹2,00,000 (~$2,400) in capital gains tax in India. You can deduct the same $2,400 from your US tax liability.

✅ This ensures that while you must report the income in the US, you won’t pay tax twice.

Conclusion: Your Repatriation Checklist & Final Advice

Step-by-Step Repatriation Checklist

- [✓] Identify source of funds: NRE or NRO.

- [✓] If NRO, ensure within $1M annual limit.

- [✓] Pay all Indian taxes (e.g., Capital Gains Tax).

- [✓] Get CA certificate (Form 15CB).

- [✓] File Form 15CA online.

- [✓] Submit docs to your bank.

- [✓] Claim FTC in your US tax return.

The Golden Rule

Repatriation involves large sums, regulatory paperwork, and dual tax systems. Always consult:

- A Chartered Accountant (CA) in India for compliance.

- A CPA in the US for DTAA and FTC filings.

Quick Summary for Readers

This guide helps NRIs bring Indian earnings back to the US legally and tax-efficiently. Key takeaways:

- NRE → simple, tax-free, no limits.

- NRO → capped at $1M/year, needs Form 15CA/CB + tax clearance.

- Common cases: property, investments, rent.

- Tax efficiency: Use the Foreign Tax Credit (FTC) to avoid double taxation.

FAQs

Q1. Can I transfer unlimited money from India to the US?

No. NRE funds are unlimited, but NRO transfers are capped at $1M per financial year.

Q2. Do I pay tax in both India and the US on the same income?

Yes, you must report in both, but the India–US DTAA allows you to offset with the Foreign Tax Credit.

Q3. Do I need RBI approval for repatriation?

Not usually. Most transfers are bank-processed with Form 15CA/CB. RBI approval is needed only in exceptional cases.

Q4. Is gift money or inheritance treated differently?

Inheritance is allowed, but proof of succession and taxes must be cleared before transfer.