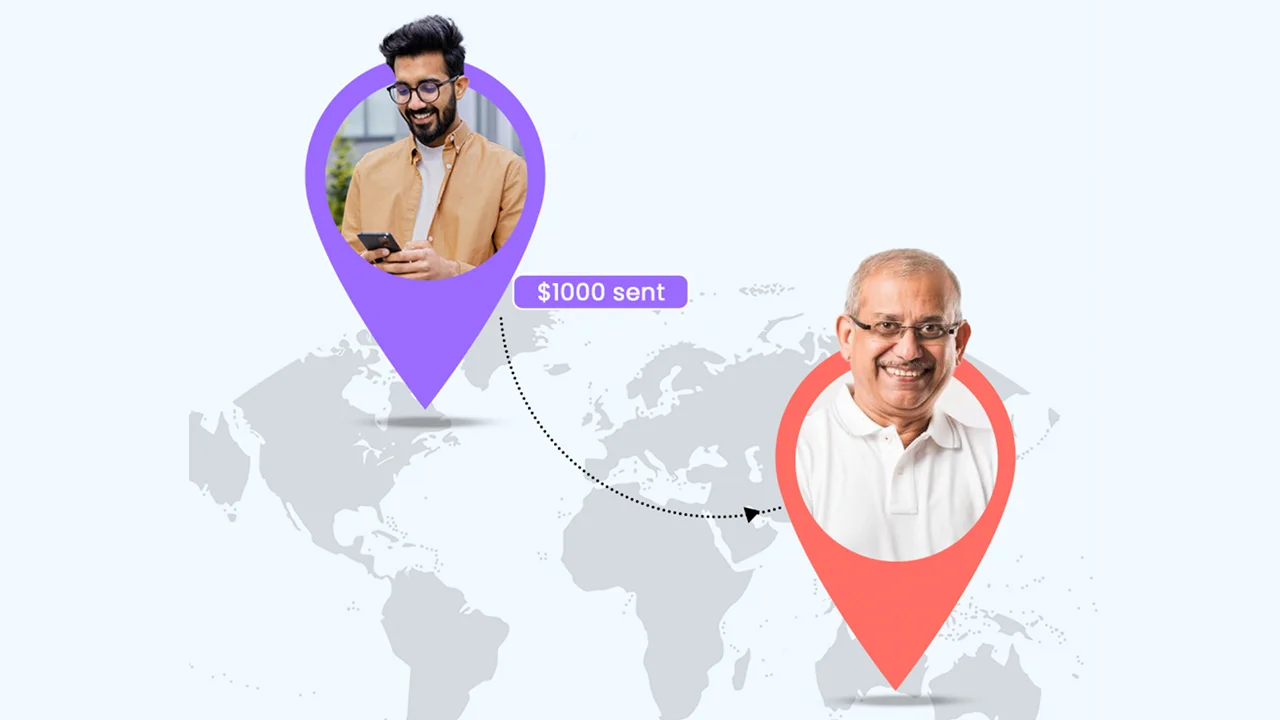

In today’s globalized world, the need for seamless financial transactions across borders has become paramount. International remittance, the process of transferring funds from one country to another, plays a crucial role in facilitating cross-border payments. Whether you’re supporting family members abroad, paying for goods or services, or investing internationally, understanding the basics of remittance is essential for efficient financial management.

Different Types of International Remittance:

International remittances can take various forms, each with its own set of advantages and considerations. Some common types include:

1. Wire transfers: These electronic fund transfers allow for the rapid movement of money between banks or financial institutions across borders.

2. Online money transfers: Services like Western Union, MoneyGram, and Wise (formerly TransferWise) enable individuals to send money internationally through digital platforms.

3. Remittance cards: Prepaid cards can be loaded with funds in one country and used for withdrawals or purchases in another.

4. Mobile money transfers: With the rise of mobile banking, remittances can be initiated and received using mobile applications.

5. Cryptocurrency remittances: Digital currencies like Bitcoin offer an alternative method for borderless financial transactions.

Difference Between Payment and Remittance:

While payments and remittances are often used interchangeably, they are distinct concepts. A payment refers to the transfer of funds in exchange for goods or services, whereas a remittance is the act of transferring money from one party to another, usually across international borders, without an immediate exchange of goods or services.

Example of Remittance:

A common example of remittance is when an expatriate worker sends a portion of their earnings back to their home country to support their family. This act of transferring funds from the host country to the home country is considered an international remittance.

Remittance Fees:

When sending money internationally, fees are often involved. These fees can vary depending on the service provider, the amount being transferred, and the destination country. Common remittance fees include:

1. Transfer fees: A flat fee or percentage of the transfer amount charged by the remittance service provider.

2. Exchange rate markups: The difference between the interbank exchange rate and the rate offered by the service provider.

3. Receiving fees: Some institutions or services may charge a fee for receiving the remitted funds.

4. Additional fees: Fees for services like cash pickup, home delivery, or expedited transfers.

How to Avoid TCS on Foreign Remittance:

In India, the Tax Collected at Source (TCS) is applicable on foreign remittances exceeding a certain threshold. To avoid TCS on foreign remittances, you can:

1. Provide proof of remittance for specific purposes like education, medical treatment, or travel.

2. Utilize the Liberalized Remittance Scheme (LRS) limit, which allows for tax-free remittances up to a specified amount per financial year.

3. Remit funds through authorized channels and maintain proper documentation.

Benefits of Foreign Remittance:

Beyond facilitating financial transactions, international remittances offer several benefits:

1. Economic support: Remittances provide a vital source of income for families and communities in developing countries.

2. Improved living standards: Funds received through remittances can be used for education, healthcare, and other essential needs.

3. Investment opportunities: Remittances can be channeled into productive investments, fostering economic growth and development.

4. Promotion of financial inclusion: Remittance services often reach underserved populations, increasing access to financial services.

Conclusion:

Understanding the intricacies of international remittance is crucial for individuals, businesses, and economies alike. By navigating the various options, fees, and regulations, you can ensure efficient and cost-effective cross-border fund transfers. As the world becomes increasingly interconnected, the ability to send and receive remittances seamlessly will continue to play a vital role in fostering global financial inclusion and economic development.

FAQs:

1. What is the difference between inward and outward remittance?

Inward remittance refers to funds received from abroad, while outward remittance involves sending money to a foreign country.

2. Can I send remittances for any purpose?

While remittances can be sent for various purposes, some countries may have restrictions or regulations regarding the reasons for remittance, such as prohibited activities or limitations on the amount.

3. How long does an international remittance take?

The time it takes for a remittance to be processed and credited can vary depending on the service provider, the countries involved, and the method of transfer. Generally, wire transfers are faster than traditional money transfer services.

4. Are remittances taxable?

The taxation of remittances depends on the country’s laws and regulations. In some cases, remittances may be subject to taxes or reporting requirements, especially if the amounts are significant or if the funds are used for specific purposes.

5. Can I remit funds anonymously?

No, most remittance service providers require identification and documentation to comply with anti-money laundering and counter-terrorism financing regulations. Anonymous remittances are generally not permitted.

By addressing these common questions, you can gain a better understanding of the nuances involved in international remittances and make informed decisions when sending or receiving funds across borders.