As an NRI, you diligently save money in your Indian NRO (Non-Resident Ordinary) account. But when you check your statement, you notice a significant chunk of your interest income is missing.

The culprit? TDS (Tax Deducted at Source).

For many NRIs, TDS on NRO accounts is a major point of confusion—and often, financial loss.

This guide will demystify NRO TDS in 2025. We’ll cover:

- What it is and why it’s deducted

- The current TDS rate for NRIs

- Step-by-step strategies to minimize deductions and maximize savings

First, A Quick Refresher: What is an NRO Account?

An NRO (Non-Resident Ordinary) account is designed for NRIs to manage income earned in India, such as:

- Rent from property

- Dividends from stocks

- Pension

- Other Indian-sourced earnings

Key Point: The interest earned in an NRO account is taxable in India.

👉 Contrast: An NRE (Non-Resident External) account holds foreign earnings. Its interest is tax-free in India and fully repatriable.

What is TDS, and Why is it Deducted from Your NRO Interest?

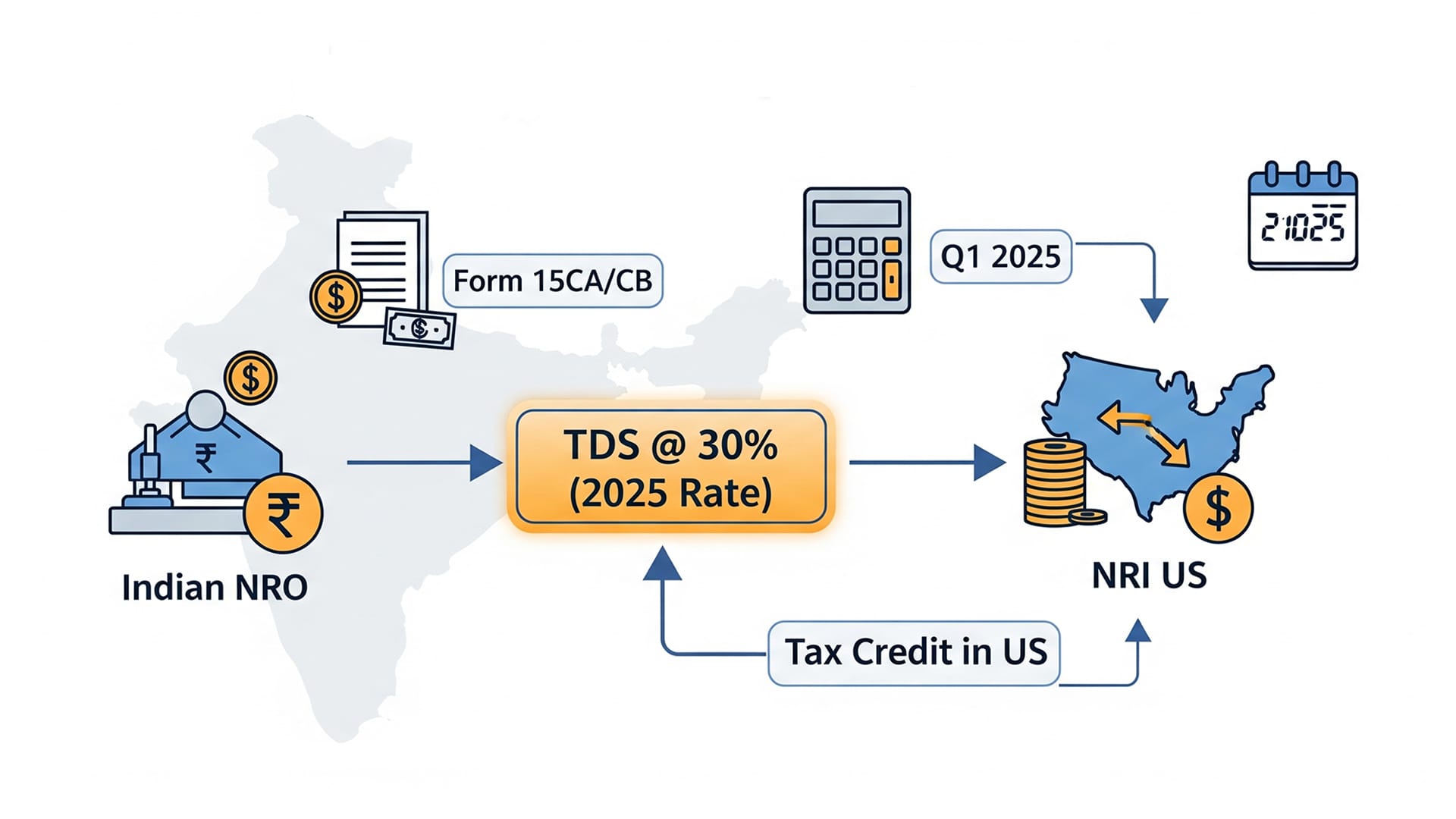

TDS (Tax Deducted at Source) is an advance tax the bank deducts before crediting your NRO account interest.

Why? Because under the Indian Income Tax Act, interest from NRO accounts is taxable for NRIs, so the bank (payer) is legally required to deduct tax upfront.

👉 In short: TDS ensures the government collects tax in advance, even before you file returns.

The Critical Numbers: Current TDS Rate on NRO Interest (FY 2024–25)

- Default Rate: 30%

- Surcharge + Health & Education Cess: Pushes the effective rate to 31.2% (and higher for high-income slabs).

Example:

- Interest earned: ₹10,000

- TDS @ 30% = ₹3,000

- Health & Education Cess (4%) = ₹120

- Total Deducted = ₹3,120

👉 That’s almost one-third of your earnings gone!

The Solution: 3 Proven Methods to Minimize Your TDS Deduction

The 31.2% rate is the default—but you are not stuck with it. Here are three legal ways to reduce or recover excess TDS.

Method 1: Submitting Form 15G / 15H (For Zero TDS)

What they are:

- Form 15G: Self-declaration for individuals below 60 years.

- Form 15H: For senior citizens (60+).

By submitting these, you declare that your total Indian income is below the basic exemption limit and your tax liability is nil.

Eligibility Criteria:

- Must be a Resident Indian for tax purposes (⚠️ Most NRIs won’t qualify—only those who changed residency status).

- Total income in India < ₹2.5 lakhs (2025 exemption limit).

- Tax on total income = Nil.

How to Submit:

- Download Form 15G/15H from your bank’s website.

- Fill and sign.

- Submit to every bank branch where you hold an NRO account (ideally at start of the FY).

Method 2: Leveraging the DTAA (For Lower TDS)

DTAA (Double Taxation Avoidance Agreement) prevents you from being taxed twice on the same income. India has DTAA with 90+ countries, including the USA, UK, Canada, UAE, Australia.

- Under DTAA, banks deduct TDS at reduced rates (10–15%), not 31.2%.

Documents Needed (Checklist):

- ✅ PAN card

- ✅ Tax Residency Certificate (TRC) from your resident country (e.g., IRS issues for US residents)

- ✅ Form 10F (filed online on the Indian IT portal)

- ✅ Self-declaration of non-residency and beneficial ownership

👉 Example: A US-based NRI provides TRC + Form 10F → bank deducts 10% TDS, saving 21.2% instantly.

Method 3: Filing an Income Tax Return (ITR) to Claim a Refund

If your bank already deducted TDS at 31.2%, you can:

- File an ITR in India to report your actual tax liability.

- Claim a refund of the excess tax paid.

Steps:

- Download Form 26AS to see all TDS deducted in your name.

- File ITR online before the deadline.

- Claim a refund for the excess deduction (processed by the Indian IT Department).

👉 Practical Tip: If you frequently remit, DTAA paperwork upfront is easier than refunds later.

Summary Table: TDS Scenarios at a Glance

| Scenario | Action Taken | Resulting TDS Rate |

| Default | No action taken | 31.2% (or higher) |

| DTAA Benefit | Submit TRC, PAN, Form 10F | 10–15% |

| TDS Refund | File ITR after deduction | Initial 31.2%, refund later |

Frequently Asked Questions (FAQ)

Q1: Is TDS applicable to the principal amount in an NRO account?

A: ❌ No. TDS applies only to interest earned, not the principal.

Q2: What if I don’t submit DTAA documents?

A: The bank deducts at 31.2%. You can later claim a refund via ITR.

Q3: Do I need a Tax Residency Certificate (TRC) every year?

A: ✅ Yes. TRC is valid for one financial year only.

Q4: Can NRIs submit Form 15G to avoid TDS?

A: ❌ Generally no, since Form 15G/15H is only for resident Indians. DTAA is the practical route for NRIs.

Take Control of Your NRO Account

Key Takeaways:

- Default TDS on NRO interest = 31.2%.

- Reduce this legally via DTAA or ITR refunds.

- Always monitor your Form 26AS to track TDS credits.

By taking these steps, you move from being a passive saver to an informed investor in control of your Indian finances.